Focus On: Resins

Monthly spotlight centered on a key industry topic.

Global Coating Resins Market Trends, Sustainability Drivers and Emerging Industry Opportunities

Credit: enriscapes / iStock via Getty Images Plus

By MarketsandMarkets

Resins bind the coating ingredients together and enable them to stick to the surface to which the coating has been applied. They determine the performance of the coatings and appearance characteristics such as water or scratch resistance, ability to protect against corrosion, and gloss or matt finish.

The global coating resins market size was USD 44.7 billion in 2023 and is projected to reach USD 57.3 billion by 2029. It is projected to register a CAGR of 4.8% between 2024 and 2029. The market growth is primarily triggered by increased demand from the construction and automotive industries, a surge in investments in the infrastructure sector, demand for eco-friendly coating systems and a rise in consumers’ purchasing power. Architectural coatings are expected to generate continuous bulk demand for coating resins because of developments in the construction and industrial sectors. Market restraints include low availability and high cost of specialized raw materials needed for specific coatings and economic slowdown in European economies.

Drivers, Restraints, Opportunities and Challenges in Coating Resins Market

The global coating resins market is witnessing high growth on account of increasing applications, surging advancements in powder coating technologies and growing demand in the Asia Pacific region. Asia Pacific is the fastest-growing coating resins market due to the region's rapid growth in infrastructural activities, availability of raw materials, low-cost labor, increasing trade relations with other regions and private sector involvement. The growing population and rapid urbanization in the emerging economies of the Asia Pacific also contribute significantly to market growth. In developed regions such as North America and Europe, the constant rise in passenger car ownership drives the automotive coating resins market.

Coating resins are primarily used in architectural coatings and industrial coatings applications. The rapid growth of the coating resins market is driven by the growing demand from the construction and automotive industries. Environment-friendly characteristics, durability and better aesthetic appearance drive consumption in various applications. Increasing investments in emerging markets and less regulated regions provide growth opportunities for market players. However, stringent and time-consuming regulatory policies pose significant challenges.

The market has experienced a shift in demand from solventborne coatings to environmentally friendly products such as waterborne, powder, high-solids and ultraviolet/electron beam (UV/EB)-curable coatings (which do not contain solvents that evaporate during the curing phase and only need special ultraviolet light to cure instantly).

Thinking About Replacing PFAS in Your Formulation?

Silicone-based compounds reduce surface tension to 20 mN/m, provide water/glass contact angles of 115˚, and, based on new data, can offer oil repellency. Based on these properties, silicone compounds are a natural fit for many PFAS applications.

The producers of coating resins operate globally; many produce a wide range of chemicals. The major players in the global coating resins market are Dow Inc. (United States), Allnex (Germany) (parent company PTT Global Chemical), Arkema SA (France), BASF SE (Germany) and Covestro (Germany). The growing consolidation in the coatings industry has impacted resin producers. As several small and medium-sized coating resin producers are acquired or merged with bigger players, the number of companies in the market continues to shrink. For example, in April 2021, Covestro concluded the acquisition of the Dutch company Royal DSM's business, Resins & Functional Materials (RFM). The deal received regulatory approval after Covestro and DSM signed an agreement in late September 2020. The transaction expands Covestro's portfolio of sustainable coating resins, making it one of the world's leading providers in this market. The purchase price of USD 1.8 billion reflects an attractive 5.7x enterprise value (EV)/earnings before interest, taxes, depreciation and amortization (EBITDA) 2021, including future synergies.

Figure 1. Drivers, restraints, opportunities and challenges in coating resins market.

- Increasing demand from construction and automotive end-use industries

- Growing trend toward sustainable and eco-friendly coating systems

- Availability of durable coatings with better performance and aesthetics

- Growing consumer preference for sustainable coatings and recycled products

- Raw material volatility and geopolitical influences

- Stringent environmental regulations impacting market growth

- Fluctuations in crude oil and energy prices

- Increasing significance of biobased resins in coatings industry

- Growth potential in less regulated regions

- Attractive prospects in shipbuilding and pipeline industries

- Technological sifts demand constant growth and innovation

- Recycling and waste disposal challenges

- Reduced exports from European economies

Source: Secondary Research, Interviews with Experts, and MarketsandMarkets Analysis

Some large coating companies produce a part of their demand for resins in-house. In general, the proportion of in-house use of resins depends on various factors such as corporate policies, production schedules, and market dynamics or pricing signals created as a result of changing supply and demand levels in a given market. More specifically, if a coating resin is of strategic value to a coating company, it is used in-house only and not sold in the open market. Many small and medium-sized coating companies produce only a small portion of their demand for resins in-house. They are, therefore, dependent on distributors for most of their remaining requirements.

Coating resins are among the essential raw materials for the coatings market and are vital for applications in various industries such as construction, automotive, marine and general industrial. They are growing significantly due to technological improvements and the demand for environmentally responsible solutions in high-performance, long-lasting, and sustainable coatings.

The market is being driven by rising end-use industry demand as well as consumer demand for ecologically friendly and sustainable coatings. The availability of durable, high-performing coatings that improve appearance and meet consumer requirements for recycled and sustainable products is driving market expansion. The need for coatings that provide long-lasting performance and ease of application, stringent environmental regulations, and the need to lower system costs are all factors driving this trend. These are the main causes of the market's expansion. Biobased resins are expected to find greater market acceptance globally during the forecast period. The volatility in crude oil prices and demand from other industries using biobased resins are exerting rising pressure on raw material prices, eventually leading to the substitution of many major resins such as epoxy, polyurethane, acrylic, alkyd, and vinyl by other resins such as cellulose, phenolic and rubber-based polymers.

Extend asset life with Tetrashield™ protective resins

Cut recoating cycles and help ensure regulatory compliance with Eastman’s Tetrashield™ PC4000. This TMCD‑based, solvent‑borne 2K resin delivers FEVE‑comparable weathering performance, broad formulation compatibility, and an ISCC‑certified recycled‑content option. Learn more about PC4000’s proven weathering data below.

Credit: adventtr / E+ via Getty Images

Industry experts have generally identified resins as having the greatest potential for replacement with biobased solutions. Biobased resins are partially or completely based on monomers derived from biological or natural sources. The acute health hazards of solvent-based systems include headache, dizziness and light-headedness, progressing to unconsciousness and seizures. Irritation of the nose, eye and throat are some other effects of working with these systems. VOCs present in paint systems are harmful to the environment as well as humans. For this reason, formulating coatings with biobased resins (binders) further reduces the fossil content of the coating by replacing the petrochemical-based resin with a biobased alternative. The biobased substance of a material can be determined using the carbon dating method. This method measures and compares the ratio of Carbon 14 (C14) to Carbon 12 (C12) in the material. Material derived from recent biological matter has a higher ratio of C14 to C12 than material obtained from fossil sources such as coal and oil. Biobased resins can help paint manufacturers reduce their carbon footprint. Hence, the development of biobased resin systems is crucial for sustaining the market in the next few years.

Environmental sustainability is the main goal of developing green or biobased coating systems. It encompasses every node of the coating's value chain, from raw material to resin manufacturing and formulation. Fossil-based feedstocks such as oil, coal and natural gas are used in most coating raw materials. Overdependence on these resources takes a huge toll on the environment due to greenhouse gas release. Resins based on plant biomass exhibit beneficial effects when compared to their conventional counterparts. Plant-based materials such as linseed and soya oils are still used in coating formulations but in reduced amounts. These alternatives have the potential to replace conventional systems and increase the demand for greener options.

Credit: SergeyKlopotov / iStock via Getty Images Plus

Growth Potential in Less Regulated Regions

North America and Europe are highly regulated markets. Major manufacturers of coating resins based in these regions have to comply with stringent government rules and policies. However, developing regions have fewer or no rules for this market. The coatings and coating resins markets in Asia Pacific and other emerging economies are less regulated, opening up opportunities for manufacturers.

The increasing income and purchasing power in developing countries in Asia Pacific, the Middle East & Africa and South America are prompting higher investment in architectural, automobile, industrial, high-performance, packaging, woodworking and product finishes. Companies manufacturing coating resins have opportunities to capitalize on the growth of emerging economies such as China, India, Russia and Brazil. Governments in the above-mentioned countries are spending significantly in the construction, automotive, packaging and industrial sectors.

China is one of the largest economies in shipping and shipbuilding. The country has consistently supported the shipbuilding and pipeline industries by meeting their demand for powder coatings. The powder coating resins used in the pipeline industry are improving continuously. In addition to the shipbuilding industry, the use of plastic tubes is increasing in the electronics, chemicals, textiles, petrochemicals, pharmaceuticals, healthcare and urban construction sectors. This creates an attractive opportunity for the powder coating resins industry to invest in these sectors, especially in the emerging economies of Asia Pacific and South America.

The increase in demand from applications such as architecture and automotive is expected to drive the market for coating resins. The emerging electric vehicles market is also expected to change the functioning of the supply/value chain of the automotive industry, which is also expected to impact the coating resins industry.

The coating resins industry has developed an ecosystem encompassing a range of players and processes that influence the industry's growth. Producers of raw materials such as INEOS, LG Chem and ExxonMobil provide initial feedstocks such as solvents and monomers essential to the various resin chemistries. Renowned resin producers such as Dow, Covestro, Arkema and Allnex transform these raw materials into a variety of coating resins such as epoxy, polyurethanes, alkyd and acrylics. These resins are then used by formulators and coating manufacturers such as Sherwin-Williams, AkzoNobel and PPG to produce coatings for various applications in the automotive, construction, wood and marine industries.

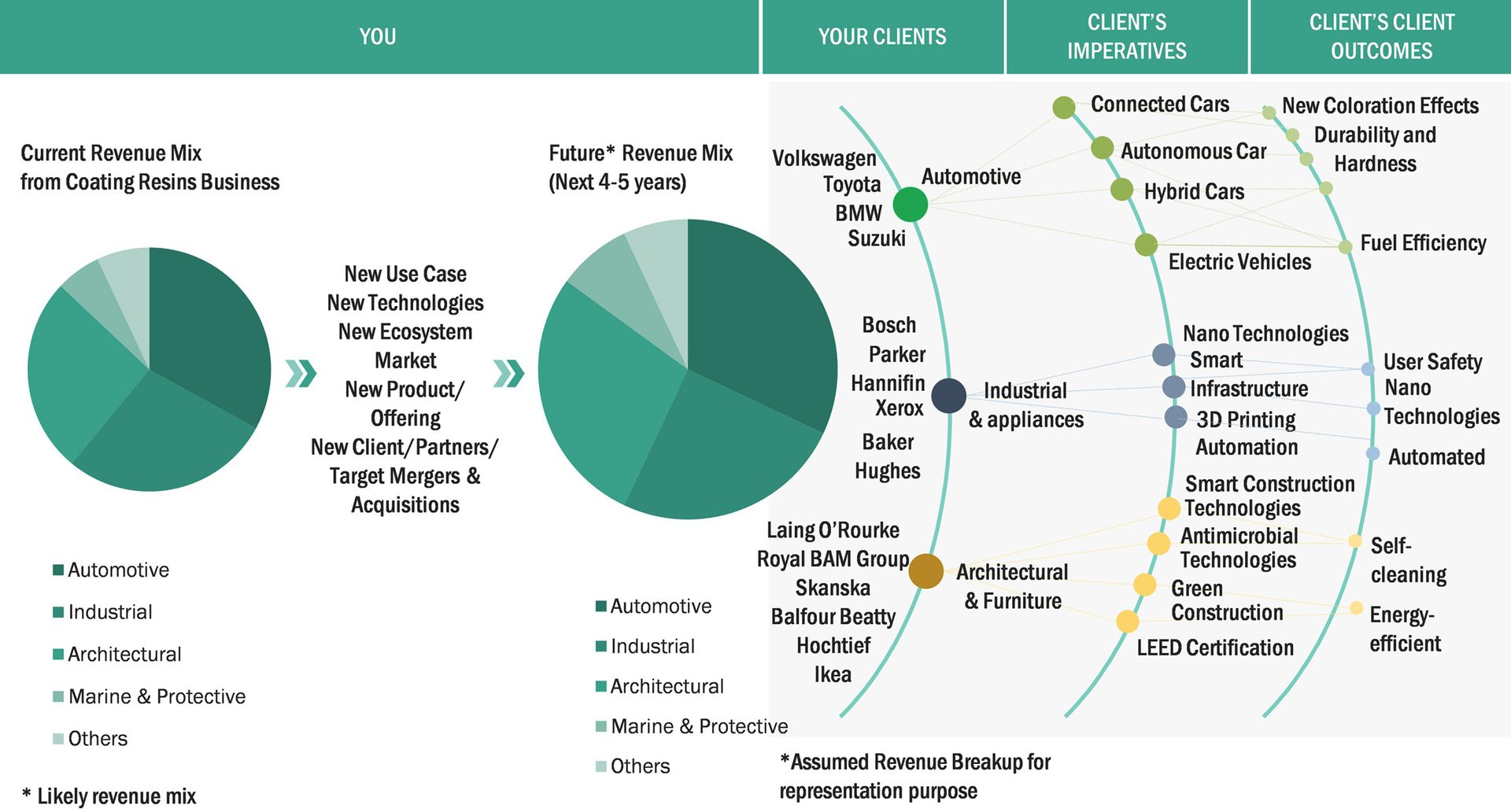

Trends and Disruptions Impacting Customer Business

Figure 2. Trends and disruptions impacting customer business.

Source: Secondary Sources and MarketsandMarkets Analysis

End-use industries have significance in coating resins utilized in the automotive industry for protection and aesthetics, the packaging industry for functional purposes, and the industrial and marine sectors for their anti-corrosive qualities. Distributors and retailers manage product flow throughout various regions through networks of distributors and retailers. At the same time, R&D centers strive to improve supply chain technology by developing high-performance, UV-cured, biobased resins that meet modern environmental demands and performance standards. This relationship between the various stakeholders and processes determines the trends, challenges and opportunities in the coating resins market.

Access the full report and learn more here.